By Philipp Buschmann, CEO and Co-founder of AAZZUR

There’s an old saying: just because you can do something, doesn’t mean you should. This has never been more relevant than when companies consider creating their own financial tech from the ground up.

Currently, businesses across various sectors, from retail to telecommunications, are eager to provide financial products to their customers. Offering financial services can significantly enhance value, whether through payments, lending, insurance, or embedded banking. The challenge? Many firms believe they need to construct their own infrastructure to succeed.

On the surface, this approach seems appealing—complete control, a tailored system, and something entirely unique to your brand. However, the reality is that developing financial technology in-house can be an expensive, complicated, and resource-draining endeavour. Even worse, if not executed correctly, it can jeopardise the business.

Rather than taking on this risk, companies should consider partnering with fintechs that have already navigated these challenges. Here’s why.

Financial Tech Is Complicated – And Expensive

There’s no denying it: financial services are heavily regulated, highly technical, and constantly changing. Even established banks, with their substantial resources and years of experience, find it difficult to keep pace.

If you’re contemplating building your own financial tech stack, think about this:

- You’ll need banking licenses (or at least partnerships with licensed institutions).

- You’ll have to adhere to KYC, AML, and a myriad of regulatory frameworks, which differ from one country to another.

- You’ll require a team of specialists, from compliance officers to fraud analysts, who grasp the complexities of financial infrastructure.

- Then there’s security, risk management, and fraud prevention—all essential yet incredibly intricate to implement effectively.

And that’s just the initial launch. Maintaining and scaling the system presents an entirely different set of challenges.

Large banks invest hundreds of millions each year just to keep their technology operational. Monzo, Revolut, and Starling didn’t emerge overnight; they dedicated years to refining their systems, continuously adapting to meet regulations and customer needs. If financial technology isn’t your primary focus, attempting to develop it on your own can lead to wasted resources, delayed launches, and a higher chance of failure.

Customers Expect Seamless Experiences—And They Won’t Wait

Consumers are indifferent to whether your financial services are developed internally or through a partner. What truly matters to them is the ease of use, speed, and trustworthiness of the service. If you create a cumbersome, slow, or frustrating system, they will leave in an instant. There are plenty of excellent alternatives available that will capture their attention. This is why collaborating with a fintech partner is so advantageous. Rather than spending years constructing your own system, you can quickly and seamlessly integrate top-tier financial solutions. Consider Tesla as an example. When they aimed to offer insurance products to their customers, they didn’t invest years in creating a comprehensive insurance platform from the ground up. Instead, they teamed up with specialists, utilizing existing infrastructure while concentrating on their core competency: manufacturing and selling cars. This principle applies to retailers, telecom companies, travel brands, and even SaaS providers. Incorporating financial services is beneficial, but it only succeeds if the customer experience is smooth, intuitive, and dependable.

Regulation is a Minefield—Fintech Partners Help You Navigate It

When launching financial services, compliance is essential. However, keeping up with constantly evolving regulations requires full-time attention, a task that fintech partners are already managing for you. The penalties for non-compliance can be severe, not just a minor inconvenience. In recent years, regulators have intensified their scrutiny and companies that neglect compliance risk losing their licenses, facing hefty fines, or, even worse, damaging customer trust. A fintech partner can help you navigate these complexities effectively as they already have the expertise, systems, and safeguards in place to ensure everything stays compliant. They deal with the technical, legal, and regulatory headaches so you don’t have to.

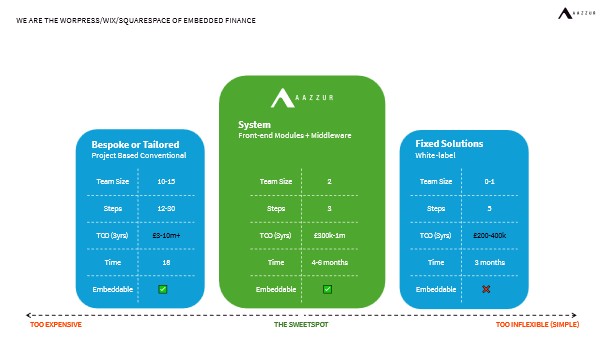

Ultimately, partnering with a fintech simplifies the process. The diagram below shows how fintech AAZZUR provides the connectivity and experience layer. It’s worth noting that you will need to add 2-3 years if you also want to do all of your own licenses and connection to the payment rails, a timeframe most businesses cannot afford.

Fintech Partnerships Save Time, Money, and Risk

Building your own financial infrastructure is akin to trying to create your own power grid instead of simply connecting to the existing one. It’s unnecessary, costly, and likely to fail. By collaborating with a fintech, you bypass years of development and can launch a solution that’s already proven in the market. This approach is quicker, more affordable, and minimises risk overall. The future of financial services lies in collaboration, not in doing it all yourself. Companies that leverage fintech partnerships will excel in speed, cost efficiency, and customer satisfaction. Those who choose to build everything from scratch? They might not last long enough to reap the rewards. The decision is clear. Adapt, integrate, and scale—or risk going under before you even begin.